2025 1st quarter investment bulletin

EXECUTIVE SUMMARY

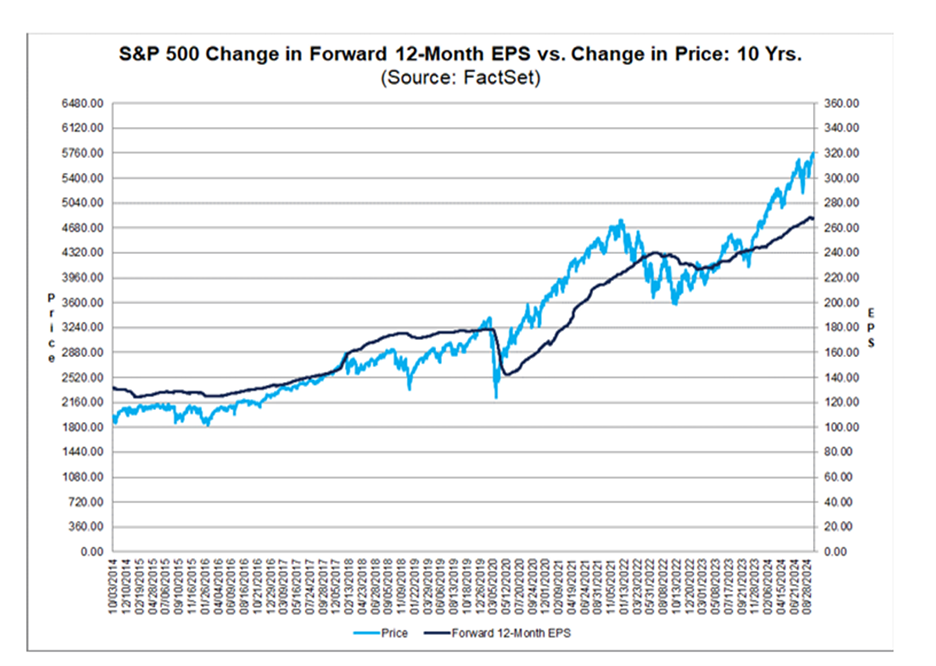

The U.S. stock market rally powered forward in 2024. The S&P 500 has increased more than 20% in back-to-back years.

U.S. Stock gains remain concentrated, large-cap stocks dominated in 2024, especially growth and technology stocks, and more specifically the so called Magnificent 7 stocks.

The strong stock market performance has led to historically high valuations.

Diversification and rebalancing in the face of persistent and concentrated gains is challenging, but necessary. Patterns of boom and bust have persisted in stocks, with the last boom pattern from 2019-2021 leading to significant downside in 2022.

Interest rates have acted uncharacteristically since the Federal Reserve (Fed) began cutting interest rates in September. The Fed has lowered the overnight lending rate by 1% and despite those rate cuts, the 10-year Treasury rate has risen 1%.

Potential policy changes related to tariffs and deportation have stoked fears of a resurgence in inflation. This seems likely to be the cause of the strange interest rate reaction in the bond market. The bond market is likely concerned that a Fed pause, or reversal in interest rate policy may become necessary.

The increase in longer term interest rates during the last 4 months negatively impacted bond performance in 2024. The bond market had performed well prior to the Fed rate cuts.

Price Gains Lead to High Valuations

The gains in stock prices during the last two years have resulted in a price to earnings ratio for the S&P 500 that is 21.47. The chart below shows the histrocial price to earnings ratio for the S&P 500. The price to earnings(P/E) ratio measures how much investors are paying for every $1 of earnings that a company or the market is generating. Higher P/E ratios mean that we as investors are paying increasingly more for the earnings that stocks are generating. You can see that a price to earnings ratio of 21.47 is well above the 30-year average of 16.86. The extraordinary performance of top S&P 500 stocks is an extra source of concern for continued market strength because the valuations are more extreme in the stocks that have most significantly powered the rally. The market as a whole appears overvalued, but the top 10 stocks appear most susceptible to price declines. There are a large number of stocks that still have reasonable valuations.

Source: JP Morgan

In the short-term, stock prices can and often do continue to move higher even with higher P/E ratios. Upward momentum can push stocks higher despite being expensive. However, market history has shown us that eventually price relative to earnings wins out. The result is usually a market decline to bring price and earnings into a better equilibrium. The chart below illustrates the diminished future return prospects when starting with higher P/E ratios. The vertical column on the left of both charts shows the total return of the S&P 500 and the horizontal axis is the starting P/E ratio for the market. Higher P/E ratios indicate an expensive market and you can see that returns over both 1-year and 5-year periods are muted when starting from an expensive position. Conversely, when you measure from a lower P/E ratio, the return profile improves markedly.

It is the back and forth between gains and losses that make rebalancing so important in the pursuit of strong returns with a focus on downside loss mitigation. The act of discplined rebalancing forces partial selling of stocks into strength and partial buying into weakness. The speed at which markets move from gains to losses, and vice-versa necessitate being early in rebalancing efforts.

Source: JP Morgan

Current Positioning and Outlook

As the market continues to make new highs it is critical to partially sell into strength. In late December, many accounts were rebalanced in such a way that slightly reduced stocks and attempted to put more conservative stock positioning in place. We would expect to continue rebalancing to a more conservative posture in the event the stock market continues its upswing. This is similar to how we positioned accounts in the 2nd half of 2021 as new highs were achieved. Those moves towards a more conservative posture helped to minimize declines in 2022. Should that pattern repeat itself, we would then have a plan of action to move back to a more stock oriented and aggressive positioning in the face of future declines.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.