2022 3rd Quarter Investment Bulletin

Exeuctive Summary

U.S. Stocks fell -17% during the 2nd quarter of 2022

Large-Cap Growth stocks and Small-Cap stocks continued to be the hardest hit segments of the market

Bonds have not provided portfolios with the counterbalance to stock risk that has previously been the case. The continued rise in rates led to further declines in bonds during the 2nd quarter

The decline in stocks led to incremental increases in your stock allocation on three occasions for most accounts

Historical Bear Markets

Since 1950, the average Bear Market decline was approximately 30% requiring almost 2 years for values to fully recover all losses.

During the first 6 months of 2022, the Wilshire 5000 (an index of all U.S. Stocks) declined -21.5%. Large-Cap Growth stocks declined -29% and Small-Cap stocks were down -23.5%. This significant decline represents 75% of the average bear market decline since 1950.

The experience of going through a bear market is difficult and stirs up significant fear emotions. However, as we just detailed, a lot of the damage to stocks has likely already occurred. While it is certainly possible that the market could decline further, it is our opinion that the time to be significantly more defensive has passed.

Inflation, War and Political Discourse

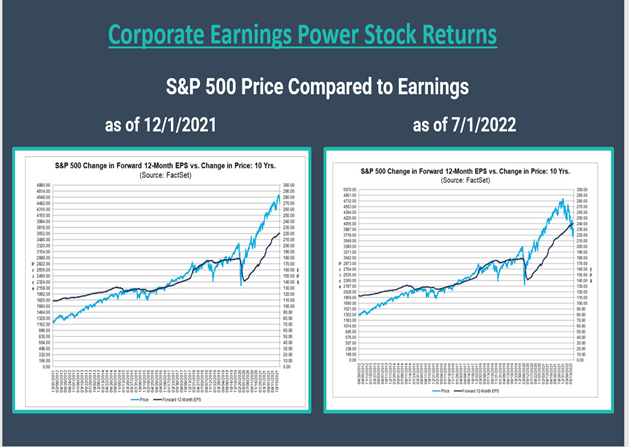

Many market pundits will draw a direct line from headline events to the decline in stock prices. While there are certainly economic impacts attributable to inflation and war in Ukraine, the primary driver for stock market movements is a company’s forward-looking earnings relative to their stock price, or their P/E ratios. The two charts below show the S&P 500 (lighter blue line) compared to expected earnings (darker blue line). The chart on the left is a snapshot from 12/1/2021, and the important item to note is that the price of the S&P 500 far exceeded earnings. This depicts an overvalued market.

The chart on the rights shows earnings in relation to the current price of the S&P 500. The lines are closer together, and earnings growth is ahead of the S&P 500 price. This chart shows a picture of a market becoming more fairly valued and possibly undervalued.

Shopping the Sale

Just as we flock to our favorite store when the items we use regularly are on sale, as stock prices fall, the case to invest becomes more compelling and ultimately rewarding. Successfully managing this requires both a diligent process and an understanding of your needs and timeframes. More recent declines have turned around rather quicky, and we have been proactive in rebalancing portfolios to try to stay ahead of a volatile market.

We hosted a market update call in May that takes a deeper dive on this subject and the overall market environment. This is a link to the presentation if you’d like to view it. Click Here

Executing the Plan

As we move through the remainder of 2022, we will continue to execute the plan that we have detailed in our communications and through our prior conversations in a rational and disciplined manner. If you feel that your individual circumstance or investment timeframe has changed since we last spoke, please let us know so we can make the necessary adjustments.