2021 2nd Quarter Investment Bulletin

Executive Summary

The first quarter of 2021 saw growth continue in U.S. Equities.

Stock prices have expanded well ahead of earnings creating pricing risk in certain market segments.

Growth stocks appear over-valued and a transition to traditional Value equities proved fortuitous.

Rising interest rates present a headwind for the bond market. Being shorter on the yield curve can help mitigate this risk.

As the economy reopens, there is capacity for employment and expanding corporate earnings. A resurgence in Covid-19 and new tax legislation may present some hurdles, but we remain optimistic.

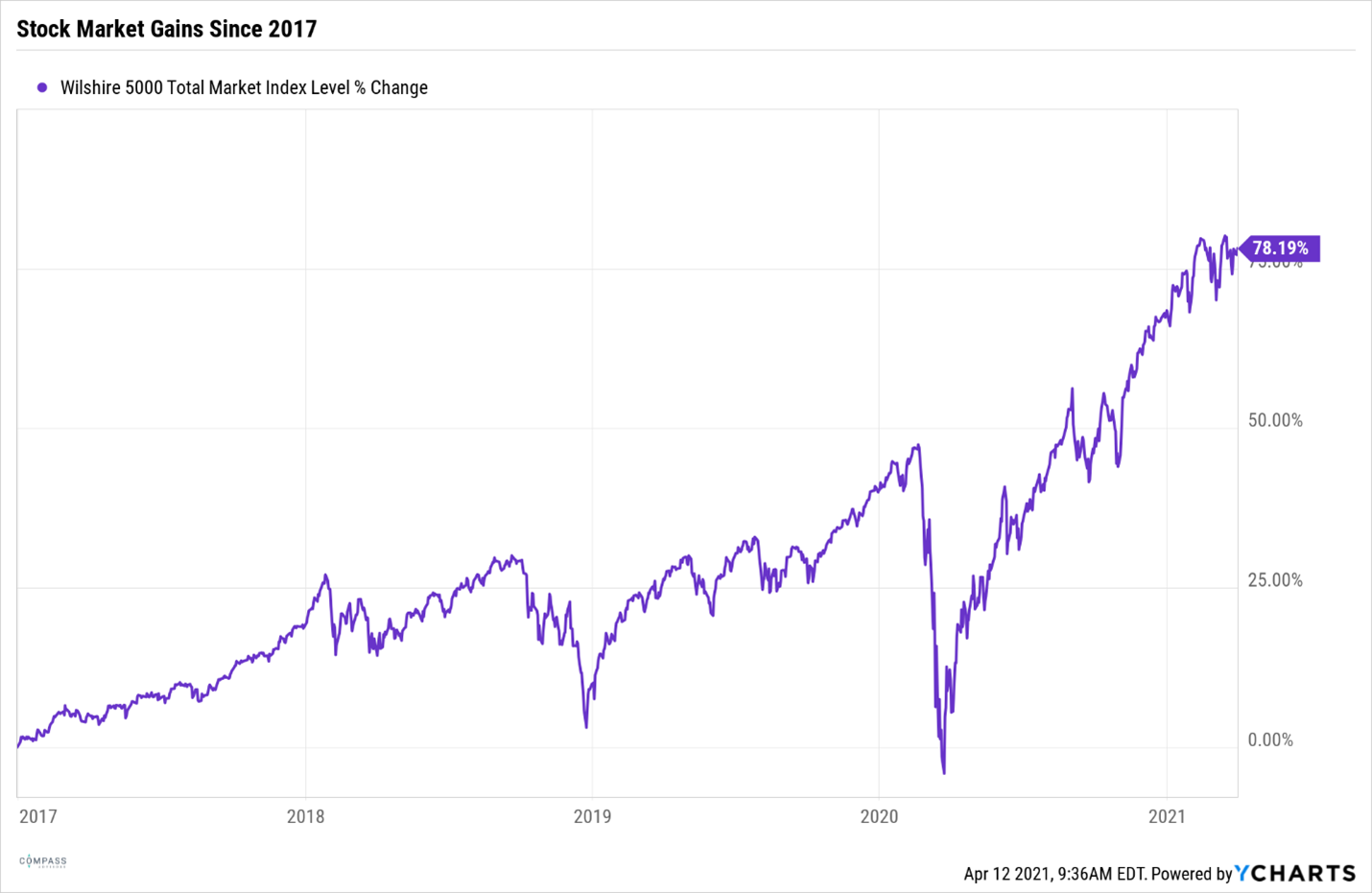

U.S. Stocks Maintain Prior Strength

The first three months of 2021 saw continued growth in U.S. equities at a remarkable pace. The Wilshire 5000 index which represents all U.S. stocks increased 6.41%. Continued expansion at that pace would annualize to a gain of more than 25%! If upside continued at that rate, the result would be market gains of more than 20% in 4 out of 5 years. The chart below shows the growth in the total U.S. stock market since 2017.

Market Gains, Profits and Price

One of the challenges that markets are inevitably confronted with following the type of significant growth we have witnessed, is lofty valuations. As price increases consistently, earnings must follow suit or investors will become concerned that the amount being paid is simply too high.

One of the measures to quantify whether a stock is expensive or not is to examine the Price to Earnings (P/E) ratio. This ratio tells investors how much they are paying for every $1 in earnings for an individual stock, or the market. Historically, the average P/E ratio has been 17 times earnings. The current S&P 500 P/E ratio is 22 based on projected forward profits. The ratio is more than 30 if the P/E ratio is calculated on trailing profits.

There has been an increase in revenue growth, but at a much slower rate than the increase in the overall market prices. Earnings growth has been approximately 15% during the last twelve months, whereas the S&P 500 has increased 60%.

Value Overweight

The increase in stock prices has led to a limited number of what would be considered bargain stocks. The overvaluation is most prominent in large companies which have growth characteristics such as communications and technology companies.

We have previously written about the concern that we have regarding the increasing concentration in a handful of names making up more and more of the S&P 500. That concern led us to shift a material portion of your allocation to what would be considered "Value" stocks. For the first time in a long time, the market leadership began transitioning slightly away from those Large-Cap Growth companies that have come to dominate the S&P 500.

Value companies, particularly smaller companies, had an exceptional first quarter of 2021. The chart below shows the performance of Value ETF's compared to the Large-Cap Growth ETF. The chart shows Large-Cap Value, Mid-Cap Value, and Small-Cap Value increasing double digits during the 1st quarter of 2021, while the Large-Cap Growth index increased only 5%.

We view the transition of market leadership from growth to value as a positive sign for the stock market. It is easier to make a case for continued upside as the gains spread between more and more companies.

Rising Interest Rates and What it Means

Bond prices came under increasing pressure during the 1st quarter as interest rates began to rise. Increasing interest rates result in falling bond prices, and vice-versa. During the first three months of 2021 interest rates rose a little less than one percent which resulted in declining bond values.

While we don't want to see losses in the safer portion of your investment allocation, there are many portfolio tools to control the amount of downside that is possible on your fixed income portfolio. The primary technique that we utilize is to shorten the average maturity or duration of your investments. We have done this in your accounts and most client accounts saw losses of 1% or less within your bond allocation.

The chart below shows the performance of fixed income investments with varying maturities. The decline in price becomes more pronounced the longer the term of the investment.

Interest Rates will Most Likely Decline if Stocks Fall

The attempt to try to time interest rates is just as futile as timing the market. Although we are cautiously optimistic about stocks, there is a likelihood of a correction of some magnitude fueled by strong gains and rising valuations. If a correction of 10%, 15%, or 20% occurs in the market, we firmly believe interest rates will fall again, which will result in rising bond prices. That interplay between asset classes is the counterbalance in risk that we hold bonds for.

The chart below shows the performance of the S&P 500 contrasted with 3 bond investments during the pandemic losses in early 2020. This pattern has held true in every meaningful market decline during the last twenty years.

It has been a rewarding time to be an investor despite the challenges that exist. Prices across all asset classes have risen substantially and the economy is beginning to recover quickly. There is massive government stimulus, renewed employment throughout the economy and an incredible amount of pent up demand. The question for the market is how much of the benefit of the coming economic recovery has already been priced in? Our hunch is quite a bit until we have earnings growth to catch up to prices for many companies.